Connector Industry Shows Resilience in a Year of Surprises

As we put the pandemic year behind us, it clear that the connector industry met the many challenges it faced with strength and turned a dire forecast into a series of rebounds and successes.

The connector industry has historically reflected significant world events, and so it came as no surprise that electronics suppliers, along with many other businesses, experienced a jolt at the beginning of the global pandemic. However, 2020 ended up being a year full of surprises. Before COVID-19 closed factories in China, Bishop & Associates started the year anticipating that connector sales would grow 3.5% in 2020. By March, however, as key economies like China and the U.S. went into lockdown, it was clear that we would need to update that forecast. Based on lengthy discussions with top management at key connector manufacturers, we revised our forecast sharply downward to reflect an anticipated decrease of 30.8% in connector sales — a decline in connector sales dollars of nearly $20 billion.

April, May, and June proved to be challenging months, with worldwide connector industry sales declining in the double digits. By September, though, sales had once again moved into positive territory, and in October, the industry recorded the highest year-over-year growth since July of 2018. At that time, based on input from key connector companies, Bishop once again adjusted its forecast, this time forecasting sales down only -9.4%, which is a far cry from the -30.8% previously forecasted!

Fortunately, the industry proved to be even more resilient than any of us had anticipated and fourth quarter 2020 proved to be outstanding, recording the highest quarterly sales in connector industry history.

Connector Markets See Uneven Rebound

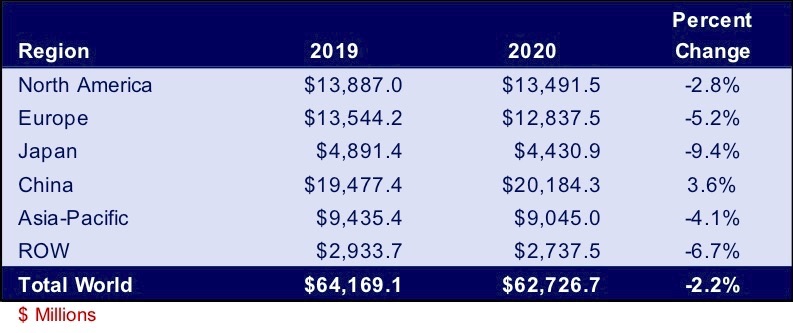

Although connector sales made a respectable rebound, the industry labored under very trying conditions in 2020, including material shortages, sick workers, sudden shifts in demand, chip shortages, and even shipping container shortages that created supply chain disruptions. Some countries fared better than others under these conditions. China’s government imposed strict restrictions on its population early in the pandemic to contain the virus, and as the world’s main manufacturer of personal protection equipment, the country’s businesses enjoyed advantageous access. China thus came out of lockdown the earliest and was the only region to see connector sales grow.

North America proved to the world that it could rapidly divert manufacturing capacity from one industry to another as businesses transitioned their assembly lines from core competencies, such as automotive assembly, to the production of medical equipment. North America saw connector sales drop modestly. Japan’s connector industry was hit the hardest, experiencing relatively steep losses.

In addition to connector sales varying by region, sales also varied by market sector as product demands changed to accommodate new usage patterns. The telecom/datacom market managed to achieve modest growth, spurred by two primary factors: increased internet activity as societies transitioned to online models of work, school, and social activities, which required new investments in infrastructure to support increased demand, as well as the continued drive towards 5G, which is creating steady demand for the equipment needed to support widespread activation of the latest generation of broadband. In line with this growth, the computers and peripherals category saw only a very slight decline in 2020, as compared to the greater sales decline observed from 2018 to 2019, due to increased investments related to telecommuting equipment.

The market sector showing the greatest decline was the automotive sector. This was primarily due to automotive plants being shuttered and most dealers being forced to close showrooms. In fact, in the U.S., 2020 saw the fourth-largest annual decline in automotive sales since 1980. What is surprising is that the industrial market, tied heavily to automotive production, saw connector sales decline only modestly, due to the repurposing of many of these factories. The transportation sector also experienced steep declines, as global travel restrictions and reduced business and leisure dampened demand. The commercial aerospace industry experienced unique business problems in 2019 that rolled over into 2020 and impacted the sales of new aircraft.

Connector Industry Forecast for 2021

So what does the forecast look like for 2021? A cautiously optimistic outlook on the pandemic is giving businesses and consumers reason to expect an accelerated return to regular activities, although some sectors will see long-term changes. Bishop & Associates anticipates that all electronic connector market sectors will grow in 2021, with the largest increase in the telecom/datacom sector.

Several factors confirm the connector industry’s anticipated growth in 2021.

- The U.S. financial markets, which had a historical contraction in early 2020, came back very strong and set new records for the DJIA and the NASDAQ. Although the markets are volatile, the growth has leveled off and is predicted to remain strong in 2021.

- The international markets have seen similar loses and recovery.

- GDP annualized growth in the U.S. is projected to be down in Q1 0.6%, but it is expected to grow between 3.4% and 3.8% in the remaining quarters. Europe is projected to be down 2.8% in Q1 and to grow between 4.0% and 12.6% in the remaining quarters. China’s GDP is expected to grow between 5.1% and 6.7% through 2021.

- Unemployment rates have been understandably high. The U.S. is expected to stay between 6.0% and 6.5% for 2021, while Europe is expected to stay between 9.4% and 9.7%, and China is expected to stay between 5.1% and 5.5%.

- The U.S. housing market has been strong since things started reopening in May and June and is partially driven by people moving out of the major cities, such as New York and San Francisco. Due to the combination of low interest rates and a significant increase in the number of people now working from home, the U.S. real estate market should continue to be strong in 2021.

- Some industries will experience long-lasting effects. Aircraft manufacturers, the airline and cruise industries, and service industries such as restaurants, gyms, and salons, to name a few, will not be quite the same for some time to come.

To see detailed facts and figures related to the connector industry’s performance in 2021 and anticipated forecast for 2022, click through to the new Bishop & Associates Connector Industry Forecast report, which includes 2022 performance in key markets and regions, and forecast commentary on end-use applications and connectivity product categories. This comprehensive, eight-chapter report also examines the larger trends and technologies that will shape connector product demand and development over the next five years. Other analysis includes a look at disruptive factors such as technology developments by market, manufacturing trends including outsourcing, and regional topics including China.

No part of this article may be used without the permission of Bishop & Associates Inc. If you would like to receive additional news about the connector industry, register here. You may also contact us at [email protected] or by calling 630.443.2702.

Like this article? Check out our other Market Update and Industry Facts & Figures articles, our 2021 and 2020 Article Archives, and our Markets Page, which features the latest articles in each of nine markets.

- Is the Gold Rush Over for China Connector Sales? - October 17, 2023

- The Top Five European Connector Suppliers for Product Quality and Price Competitiveness - October 10, 2023

- 2023 Top Five European Connector Suppliers - September 26, 2023