The Instrumentation Connector Market

It’s all about higher speeds and higher bandwidths.

As many economies begin to emerge from the pandemic, instrumentation companies are bracing for a surge in test equipment. Semiconductor companies will require testing of the latest 5G chips, and Analytical & Scientific labs are gearing up for the vast array of clinical research the pandemic has spurred. These new demands join existing needs for Test & Measurement instruments to support other fast-growing industries such as automotive, industrial, and transportation.

Instrumentation Connector Market

The instrumentation connector market consists of a broad product mix of connectors (and contacts) with increasingly higher densities and smaller form factors. These products accommodate a moderate degree of customization designed for Test & Measurement and Instrumentation (TMI) equipment with varying capabilities and increased analytics.

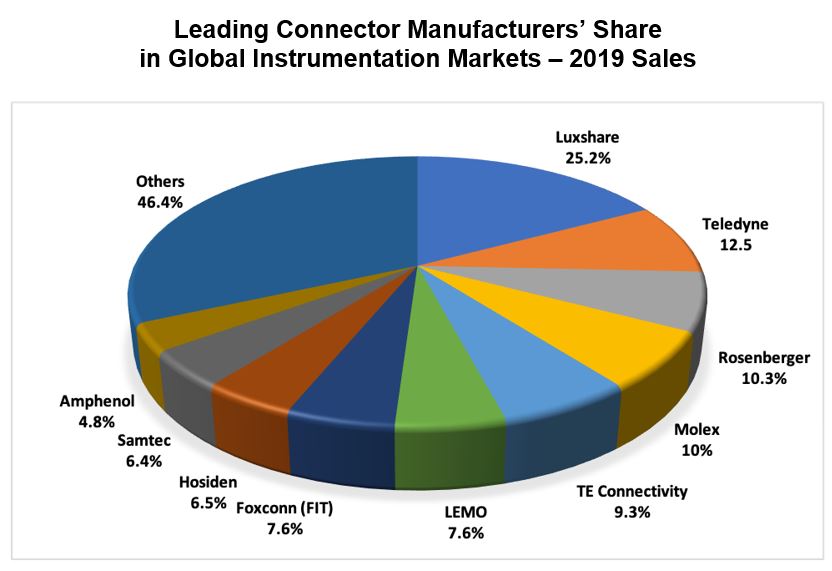

The top 10 instrumentation connector companies accounted for 53.6% of the worldwide instrumentation connector market in 2019. Each of these top 10 instrumentation connector companies offers unique and differentiated connectors designed to address specific TMI applications.

Some instrumentation equipment companies also offer connectors, such as Teledyne and Everett Charles Technologies, a Cohu company, to name a few. With Teledyne Technologies’ recent acquisition of FLIR Systems, Teledyne FLIR becomes the world’s largest instrumentation company and second largest instrumentation connector company. The latest Instrumentation Market for Connectors report highlights some of the most notable instrumentation acquisitions over the past 10 years, including mergers and acquisitions over the last 18 months.

Instrumentation connector suppliers are expanding their product offerings to align with market trends for higher density and miniaturized connector platforms that can serve emerging, fast-growing, and transformative 5G technologies, higher-speeds and bandwidths, RF technologies (including microwave and mmWave), and evolving IoT applications for a broad array of industries.

With so many new electronic-enabled devices being introduced, distribution plays a key role, ensuring efficient time-to-market by making standard connectors readily available. For lead-time reasons, more and more instrumentation customers rely on standard, readily available instrumentation connector platforms.

Among many factors, the TMI market growth will primarily be driven by growth of automatic test equipment (ATE) testing for semiconductors used for a growing number of applications, including connected car technologies, the Internet of Things (IoT), telecommunications, and industrial factory automation, to name a few.

In 2020, the total worldwide instrumentation connector market decreased 1.3% over the prior year because of the pandemic and the overall shortage of semiconductors in the supply chain, primarily affecting the automotive sector.

By 2026, we anticipate the global instrumentation connector market to exceed $2.3 billion, representing a five-year CAGR of 4.6%. China is expected to experience the highest growth, followed by North America and Japan. All other regions are expected to achieve modest positive growth levels.

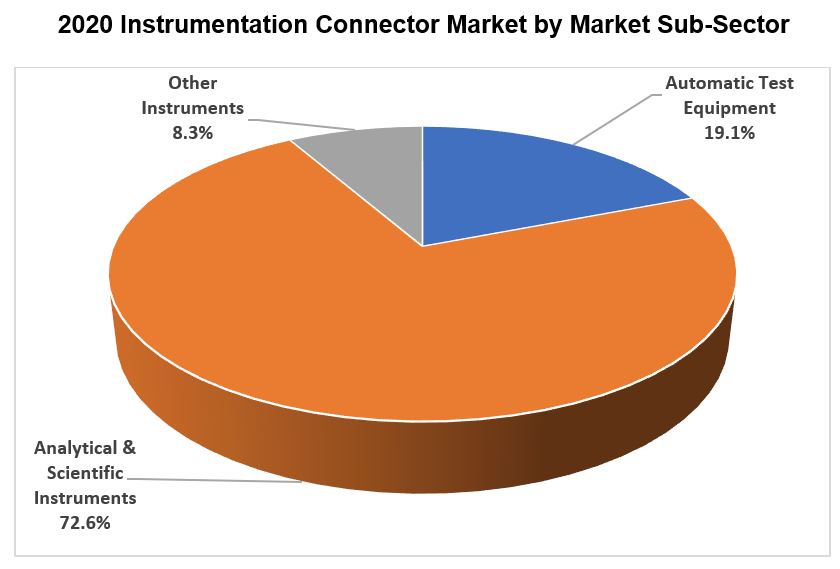

We segment the instrumentation market into three primary market sub-sectors:

- Automated Test Equipment

- Analytical & Scientific Instruments

- Other Instruments

For a detailed listing of the types of equipment that fall under each category, please visit Bishop & Associates’ comprehensive descriptions of market sectors.

All instrumentation equipment has its own technology enablers and challenging connectivity requirements that require unique connector characteristics. Bishop & Associates’ latest research report, Instrumentation Market for Connectors, provides in-depth analysis of the markets, products, and technologies of instrumentation equipment makers and provides examples of instrumentation connectors by market sub-sector for the applications they serve. Company profiles and market insights on the top 15 test, measurement, and instrumentation companies is also included.

All instrumentation equipment has its own technology enablers and challenging connectivity requirements that require unique connector characteristics. Bishop & Associates’ latest research report, Instrumentation Market for Connectors, provides in-depth analysis of the markets, products, and technologies of instrumentation equipment makers and provides examples of instrumentation connectors by market sub-sector for the applications they serve. Company profiles and market insights on the top 15 test, measurement, and instrumentation companies is also included.

In addition, the implementation of 5G higher speed and higher bandwidth technology will drive increased demand for semiconductor testing capacities. Emerging new technologies, analytical software, and technology-driven investments will offer growth opportunities in support of analytical and scientific instruments for medical life sciences. The widespread deployment of RF microwave and mmWave technology, and the continued transformation from analog to digital instruments will also fuel growth of telecommunications, consumer electronics, and autonomous vehicles.

The instrumentation connector market is transforming at higher speeds and bandwidths, which require unique connector and cabling strategies and differentiation. Gain market insights for increased participation in some of the world’s fastest growing industries, including telecommunications, consumer electronics, automotive, medical and laboratory instruments, aerospace and defense, and other emerging sectors.

Click here for detailed information on Bishop & Associates’ new Instrumentation Market for Connectors report.

Like this article? Check out our other Market Update and Industry Facts & Figures articles, our 2021 and 2020 Article Archives, and our Markets Page, which features the latest articles in each of nine markets.