Uncle Sam Wants You! (And Your Connectors!)

Uncle Sam Wants You! (And Your Connectors!)

Over the years, the level of the federal government’s involvement in the electronics industry has varied. Here, we look beyond mil/spec activity, which Connector Supplier has covered in depth, to focus on the federal government, census data, and the Fed’s actual and ideal role in advancing US global competitiveness.

Government involvement in industry has waxed and waned over the years, depending on the administration in Washington. Generally speaking, Democratic administrations and Congresses have been active, spending more on technology initiatives, but also more heavily regulating industrial activity; Republicans have been typically less proactive, viewing the marketplace, competition, lower regulation, and taxes as the best ways to unleash the forces of innovation. So, over the past 20 years or so, government policy has been consistent in some areas, such as NSF and federal lab funding, while less consistent in others.

During the Clinton years, for instance, Washington got deeply involved in funding R&D consortia via the Defense Advanced Research Projects Agency (DARPA); so much so that they changed the name to ARPA, dropping the “Defense” moniker. Government also funded the National Institute of Standards and Technology NIST (the bureau of standards before 1988) and its Advanced Technology Program (ATP), with objectives similar to those of ARPA. This writer was involved with ARPA/NIST programs, in proposal writing and as an ATP reviewer for the government. My observation was that these programs did some good by advancing new technologies, with the most important aspect being that companies, universities, and federal labs were encouraged to work together to conceive and advance a particular technology. Examples included fiber optics, light emitting diodes for illumination, MEMS technology, and high-performance computing. Some of these programs were well ahead of their time, however, and significant developments, such as in-system use of polymer waveguides and free-space optics, remain on the distant wish list, as most impetus dissolved when markets shifted and organizational re-direction occurred after the projects were completed. There is also the issue of what comes first: Government offering a funding mechanism and industry rushing in with ideas to get the funding; or industry proposing an important R&D initiative that attracts funding. I think the latter is better if at all; but from a practical standpoint, the former is more typical of how the government (and business) works.

During the second Bush administration, 9/11, wars in Iraq and Afghanistan, and homeland security issues took precedence. ARPA went back to DARPA and successfully redoubled its focus on the military and defense, including the ongoing UAV developments. The ATP program continued, but would wind down and out as the recession, domestic and defense spending, and a growing Federal budget deficit crowded out funding for such programs.

Under the Obama administration, technology initiatives have focused on new areas or increased in others, including technologies related to climate change and domestic energy development and exploration, such as the highly publicized funding of electric vehicle development, battery technologies, solar and wind energy, and other energy technology developments.

The bottom line in all these gyrations might include the following observations:

- Technology development is best left to the private sector, with government removing obstacles for companies and other organizations to work together to advance new technology. An exception is where there is a challenge beyond the scope of individual companies, beyond their Wall Street window, or where, as in the case of NASA, it is determined that funding competitive private industry developments will be more efficient than a direct government entity. One case in point is the Space Shuttle program, which was still using 20-year-old technology.

- Government funding of industrial initiatives should be carefully determined without political interference — and preferably not be past the research phase. NSF funding of university research probably has many of the same characteristics. Hundreds of university programs seek government funding, which may be ingrained in their budgetary and Ph.D. staffing processes. Government’s focus should be on grand challenges, such as interstellar space, infectious diseases, breakthroughs in domestic energy technology, or infrastructure initiatives, such as the national power grid or an ultra-wide band Internet.

- Industry does respond to enlightened government leadership, regulatory, and tax policies. More could have, should have, and can be done to promote domestic manufacturing without running afoul of industry’s role in the global marketplace. The degree to which the US has become massively dependent on foreign manufacturing, particularly in China, is an issue of monumental proportions.

- Industry can do more to promote the common good. Leaders such as IBM, Microsoft, Intel, Google, Apple, and others who are fierce competitors have done some of this; but more needs to be done. Such initiatives could be a move to manufacture major computer or mobile consumer products in the US, or a demonstration of how monolithic semiconductor manufacturing could extend into end products. Another would be to beef up export programs to reduce the current accounts deficit and lessen exposure to the vagaries of international trade.

- Industry associations, users groups, and consortia are good things and much has been accomplished through such organizations. Examples include the Semiconductor Industry Association, Sematech, ITRS, IPC, and iNEMI. The connector industry has a way to go in this regard. While some companies participate in defining industry standards, the amount of involvement has declined due to budgetary constraints. For the most part, our industry sticks close to its knitting, is very competitive, and is in the position of reacting to OEM design directions.

A Final Word About US Competitiveness

The US is doing well in the global marketplace. All other developed regions have also felt the tug of offshore manufacturing — just look at Japan or Taiwan. In fact, this has been going on for more than a decade now and has become ingrained in our industry. However, while this has become a necessity of the current global marketplace, some feel the loss of domestic manufacturing infrastructure has gone too far. This has exposed the US to an eroding manufacturing base, with fewer high-paying assembly-line jobs now and fewer high-tech jobs later, impacting consumers and the American way of life. For business, offshoring has vastly increased our exposure to crippling shortages, should there be an untoward event in Asia, and there are real risks involved in the embedding of expertise and intellectual property in offshore locations.

This is a complex issue. At the component level, where we do not control destiny, we are required to support OEM and EMS customers who assemble electronic products in China. These are then turned around and exported to the US. Many companies have been very successful in making that round trip, but one wonders: Down the road, when China’s infrastructure matures, will we be able to compete with their homegrown manufacturers whose capabilities were honed by our outsourcing? There is also the issue of taxes and regulation. Companies have moved from state to state, and now from country to country. The US currently ranks 7th in global competitiveness, behind Switzerland, Singapore, Finland, Sweden, Netherlands, and Germany. In some product areas (PCs, tablets, smartphones), nearly 100% of production is offshore. A huge amount of capital is being held and invested offshore to avoid US corporate taxes. The list goes on.

Bottom line is that modern day US competitiveness in a global marketplace means making and selling products where equipment is being manufactured. So the onus is on the OEM/EMS industry to do something about that. One potential answer is in emerging technologies; but even there, the US no longer is assured of long-term advantage. Imagine where we would be today if just a quarter of all that offshoring was still here in the US, with vibrant export programs around the world.

Some government or related organizations and initiatives that touch on the electronics industry include:

- President’s Council of Advisers on Science and Technology (PCAST). The current council is comprised of 19 science and technology leaders from industry and academia. Those from the electronics industry include Eric Schmidt, chairman of Google; Maxine Savitz, retired general manager of technology policy at Honeywell; and Craig Mundie, technology guru at Microsoft. The current council is weighted toward environmental and medical expertise. Its initiatives include climate change; networking and information technology; agricultural preparedness; US research enterprise; and drug innovation. More can be found here.

- DARPA. This agency, located in Arlington, Va., focuses on projects for defense sciences, information innovation, microsystems technology, strategic technology, tactical technology, and small business initiatives that include SBIR and STTR Innovation Research program funding. There are opportunities to get R&D funding at DARPA, but the project must be new technology, not evolution of an existing technology, and the development may need to have military/defense applications. Examples could be a micro-machined/micro-robotic connector technology or a connector technology with superconducting contacts. Go here for more info.

- National Laboratories. The Department of Energy (DOE) has 19 labs scattered around the country doing research in energy-related technologies. Prominent among these are Sandia, Lawrence Berkeley, and the new Renewable Energy Laboratory (NREL) in Golden, Colo. There are opportunities to collaborate with these labs or to do a technology transfer from them under license. Developments as disparate as MEMS technology, polymer waveguides, and flexible circuitry are nestled in the nooks and crannies of these labs. There is also some controversy in the suggestion that the money spent by the federal labs system may not have gotten, for some, an acceptable overall return and, like most other government entities, once established, they never die. One might question why, for instance, a solution has not yet been found to obtain the United States’ energy independence — except as has been initiated by the private sector. Or why, long ago, we did not develop smart grid technology and are just now pursuing it. Information about the labs can be found here.

- Departments of Army, Navy, Air Force, NASA. A wide range of R&D is conducted at the NRL in Washington, Wright Patterson AFB in Ohio, Rome AFB in New York, the Army’s Aberdeen Proving Grounds in Maryland, and NASA Langley Field in Hampton, Va. Each of these departments have many different research needs and do collaborate with industry where required. One path to these programs is through defense contractors, although the current and near-term funding will be tight. The Wright-Patterson/Rome sites can be found here.

- iNEMI. The International Electronic Manufacturing Initiative was started through a government-industry partnership more than a decade ago to strengthen North American manufacturing. It evolved of necessity into a global enterprise with mostly private sector involvement funding and a stable vision moving forward in the 21st Century. iNEMI.org publishes the biennial Electronics Technology Roadmap covering semiconductors and most other important electronic technologies, of which I do the connector chapter with input from industry. They also have a number of technology projects that may not require membership to participate. These projects include board assembly, MEMS technology, organic PCBs, packaging, test, environmental, medical, alternative energy, and optoelectronics. iNEMI’s focus is to identify and be a catalyst to bridge industry-wide technology roadblocks in these and other key technology areas. Many major OEMs and EMS firms participate as iNEMI members, with Intel being a major contributor.

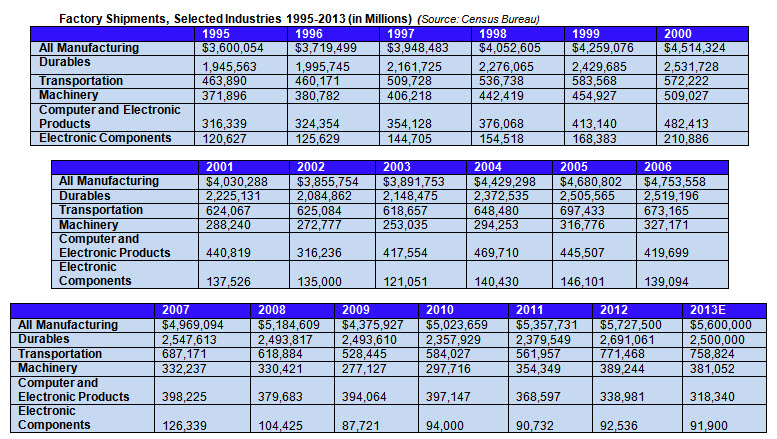

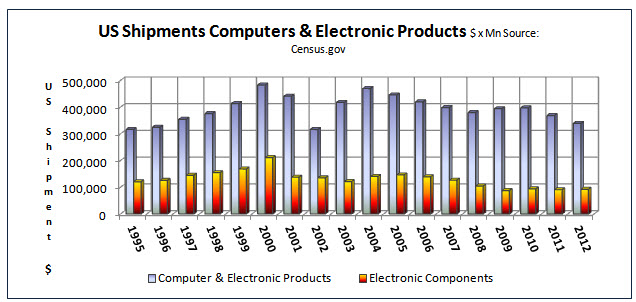

- Census Bureau. Part of the Department of Commerce, the Census Bureau was originally established to give the government statistics about the American population. Over the years, its role has expanded into all walks of life, including industry. Census and the Bureau of Labor Statistics compile detailed statistics on US production, imports, and exports of hundreds of industrial and agricultural product classifications. Most of this data is available to the general public and industry online at Census.gov. I have compiled a short list of data of interest to the connector industry; much more detailed information is available if you know where to look for it. One word of caution: Census has changed definitions over the years and you may need its help to rationalize certain data points earlier than 2007. Detailed factory shipment data can be found here.

CAGRs 1995-2012:

- All Manufacturing = 2.8% (Domestic heavy industries, chemical, food, and other manufacturing bolstered overall statistics)

- Durable Goods = 1.9% (Influenced by transportation, electrical equipment, appliances, and other domestic durables)

- Transportation Equip = 3.0%* (Transportation manufacturing growth was weak 2001-11 but bolstered by foreign implants)

- Machinery = 0.3% (Machinery data probably impacted by imports and stagnant manufacturing growth)

- Computers and Electronic Products = 0.4% (Significant growth in offshoring/imports offset US dominance in high-end technologies)

- Electronic Components = (-1.5%) (Reflects globalization and offshoring of electronic components)

* includes Asian transplant factories

Your thoughts are appreciated: [email protected].

- Electric Vehicles Move into the Mainstream with New EV Battery Technologies - September 7, 2021

- The Dynamic Server Market Reflects Ongoing Innovation in Computing - June 1, 2021

- The Electronics Industry Starts to Ease Out of China - November 3, 2020