2023 Update: How’s the Connector Industry Performing?

2023 Update: How’s the Connector Industry Performing?

The electronics industry and related supply chains are still absorbing the shocks of the pandemic era. After months of record sales, sales have entered a down cycle, yet encouraging signs are present. What do the semiconductor sales say about future sales? More importantly, what does Bishop & Associates say?

The COVID-19 era represents the wildest black swan event the connector industry has ever weathered. Factory shutdowns, stockpiling, and dramatic changes to sales activities in every market jammed up the global supply chain worse than a thousand stuck container ships. More than three years into this strange era, things have calmed down but not recovered. Concerning indicators are raising warning signs about the state of the industry, although these are tempered by positive developments as well.

Bishop & Associates just completed its research on the first quarter of 2023 (1Q23). Sales were down -0.1% versus the same period last year, which is basically flat. This is significant because 1Q23 ended 10 consecutive quarters in which the industry achieved sales growth. It is important to note that seven of the last 10 quarters achieved double-digit sales growth, as the following chart shows.

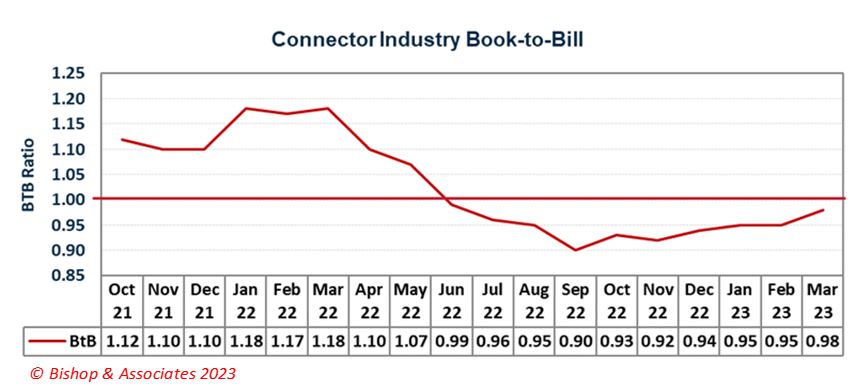

In addition to sales trending down, as shown in the above chart, orders are also declining. The connector industry has experienced a year-over-year decline in orders in 11 of the past 12 months. During the last six months this decline has been in the double digits.

Additionally, the book-to-bill ratio, as shown by the following graph, has been below 1.0 for 10 consecutive months.

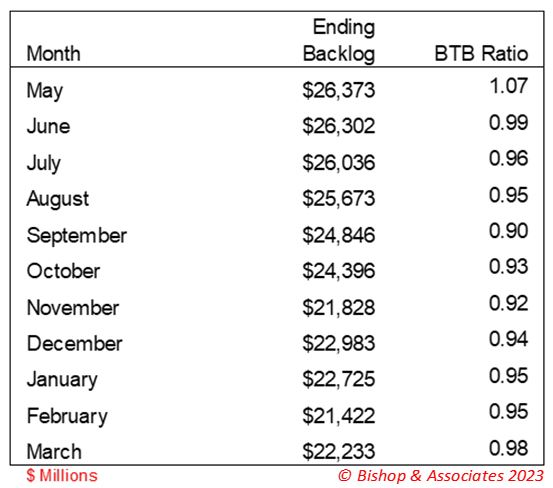

In fact, as seen in the following table, May 2022 was the last month in which orders exceed sales. And, since then, bookings have declined by $4.1 billion.

On a more promising note, we have not seen any signs that customers are cancelling orders or pushing out delivery dates.

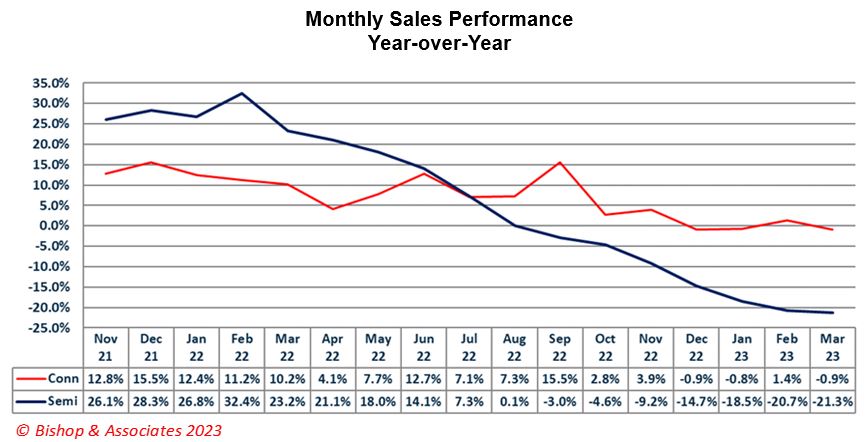

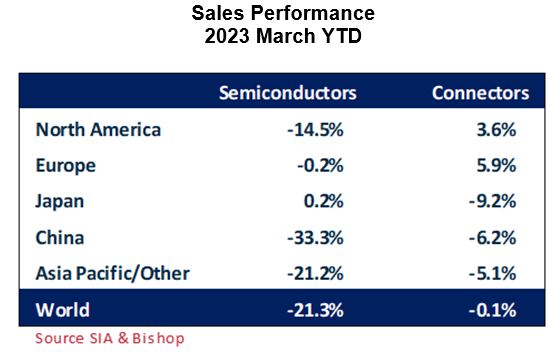

These are not the only indicators showing we are entering a down business cycle. The performance of the semiconductor industry is another good example. Historically, semiconductor sales performance leads connector sales by a few months. The following chart displays semiconductor sales versus connectors sales for the last 17 months. You will note that semiconductor sales have declined for seven consecutive months. Of these declines, four were double digits.

The following table shows year-to-date semiconductor sales down -21.3%. Unfortunately, this is not an encouraging sign for the connector industry.

Another clear sign that the connector industry is entering a down business cycle is layoff announcements from tech companies. One online tracker notes that 199,047 layoffs have already been announced in 2023, compared to 164,576 in all of 2022.

Some of the largest U.S.-based companies are reducing staff. Among these are 3M, Meta, Dell, Boeing, IBM, Google, Microsoft, etc.

Based on these signs, it appears we are entering a down business cycle in the connector industry. The question remains as to how long this cycle will last.

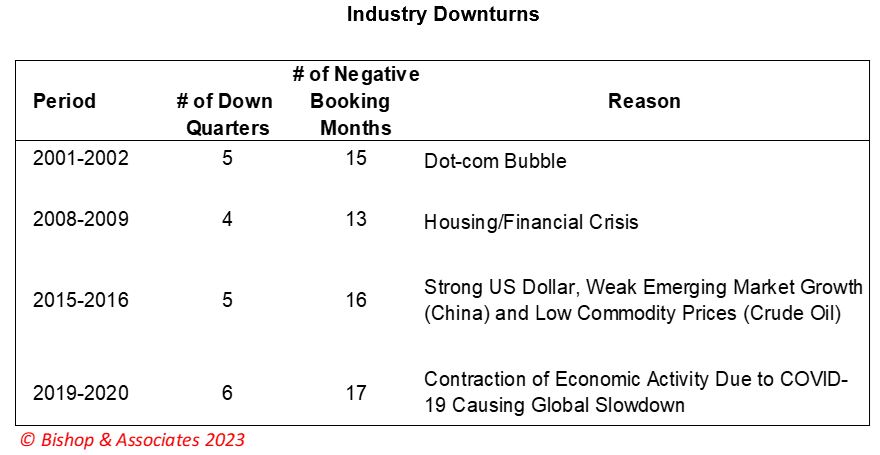

For the 21st century, we have experienced four down business cycles. The longest lasted six quarters and the shortest four quarters. The following displays the down cycles and the impact on connector sales.

Even with these clear indicators, there are also encouraging signs. First, although we have seen double-digit declines in orders, we have not seen this in sales. The performance of TE Connectivity and Amphenol, the two largest connector manufacturers, is also encouraging. Both companies achieved sales growth in 1Q23 (TE = 3.8%; Amphenol 0.7%). Further, both companies are forecasting a very modest decline in second-quarter sales, TE -2.4% and Amphenol -1.0%.

Other encouraging signs include:

- A $22 billion connector backlog that is not being affected by order cancellations or push-outs.

- An expected pause in interest rate increases.

- A strong automotive market, the largest connector end-used equipment market.

- A strong military/aerospace market.

These factors suggest that the industry will probably not experience a double-digit decline in sales. We believe it is more likely that in 2023 sales will be flat in comparison to 2022.

Bishop’s forecast is a bit more positive, with growth at +1.9%.

It is important to realize that this growth will not be the same across all regions or market sectors. The automotive and the military market are both anticipated to outperform the other sectors, while sectors like computers & peripherals, mobile phones and other data devices, and the consumer electronics market are anticipated to experience a decline.

All in all, we are not predicting that 2023 will be a disaster.

For more connector industry analysis and market research, visit Bishop & Associates.

This interview originally appeared on Samtec’s blog. See more industry insights and connectivity solutions at Samtec Inc.

Like this article? Check out our other Industry Facts and Figures articles, our Medical Market Page, and our 2023 and 2022 Article Archive.

Subscribe to our weekly e-newsletters, follow us on LinkedIn, Twitter, and Facebook, and check out our eBook archives for more applicable, expert-informed connectivity content.

- What is a Manual Service Disconnect (MSD) Connector? - August 4, 2026

- What is a Cable Tie? - July 28, 2026

- What is a MIL-DTL-28748 Connector? - July 21, 2026