Robotaxis: The Evolution from Hype to Reality

For some, the ultimate form of mobility is the robotaxi, a fully autonomous ride-on-demand vehicle that relieves passengers of the headaches of ownership. How close is this dream to reality?

It has been 100 years since Francis Houdina operated his radio-controlled automobile through New York, barreling down Broadway and Fifth Streets. While the vehicle — claimed by some to be the first “driverless” car — narrowly missed several accidents, it finally ended its history-making run by crashing into another car.

In the subsequent decades, many attempts at autonomous and semi-autonomous driving technology arose, but widespread interest did not take hold until the 1980s when the U.S. Department of Defense became involved via its Defense Advanced Research Projects Agency (DARPA). The 2004 DARPA Grand Challenge tasked engineers, students, and more to create an autonomous vehicle to navigate a desert racecourse. Though no vehicle finished the entire course, the competition validated the concept of autonomous vehicles, and companies began setting their sights on leading the charge to market. Since then, significant milestones have contributed to the evolution of autonomous driving, including Alphabet’s Waymo’s 2015 achievement of the first successful fully autonomous trip on public roads.

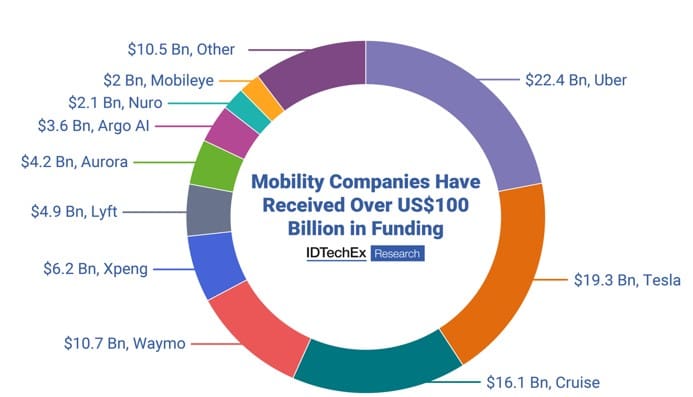

More than US$100 billion has already been spent on autonomous driving (Figure 1), the majority of which is in the robotaxi sector. However, after five years of service, operators of Level 4 robotaxis—autonomous vehicles that can drive without human intervention in specific conditions—have yet to see a profit. This article examines the dream of robotaxis and what it will take to move them from hype to reality.

Figure 1: Approximately US$100 billion of funding has gone into mobility and autonomous vehicles. (Source: IDTechEx)

Technologies Behind the Vehicles

According to research firm IDTechEx, the global robotaxi vehicle market value will reach US$174 billion in 2045 and show a 20-year compound annual growth rate (CAGR) of 37% between 2025 and 2045. The U.S. and China are expected to dominate market share. Such rapid growth requires many technologies, including radar, lidar, and ultrasonic sensors and cameras, to provide such visual data as object detection and identification of vehicles, pedestrians, and obstacles. Processors, connectivity protocols, and actuators also play important roles; more recently, artificial intelligence (AI) and machine learning (ML) enabled vehicles that tap into their experiences and complex algorithms to make sense of the volumes of data gathered.

AI and ML also improved accuracy and reliability by analyzing data in real time, recognizing potential hazards, and predicting the behavior of other drivers, all while determining the best course of action. Vehicles make informed decisions, navigate extremely tricky environments, and become increasingly proficient at navigating scenarios. This is in part thanks to global positioning system (GPS) receivers that access signals from multiple satellites to triangulate position. These data, combined with a car’s speed and direction, document exact locations in real time.

Using high-precision mapping systems, companies can provide road layouts, lane markings, traffic signs, and speed limits. Those data allow the cars to anticipate upcoming turns, intersections, and other potential obstacles to plan movements in advance. Robust software systems are implemented to detect and prevent such risks and malfunctions as errors in sensor readings and cybersecurity threats, playing a crucial role in maintaining safety.

Behind these technologies are several large companies working on autonomous vehicle technology individually and in partnership. Market leaders Waymo and Apollo have a strong reputation for their sensors, maps, and intelligence. Waymo and Baidu use complex architectures that combine several AI systems for decision-making. In comparison, Tesla uses a camera-based approach supplemented by maps and an end-to-end deep learning system that processes raw sensor data to make driving decisions. This approach has been controversial, with some experts saying it limits Tesla’s ability to achieve the precision levels seen by its competitors.

As autonomous vehicles take to the road, commercial driverless robotaxi services are gaining momentum in the U.S. and China. Key players in these regions include Alphabet’s Waymo, Baidu’s Apollo Go, and Amazon-backed Zoox, with the number of providers and locations increasing annually.

Roadblocks to Adoption

While technological precision potentially translates to lower accident rates than human-driven cars, challenges exist. Regulatory and legal challenges, safety, data privacy, accident liability, and system certification are necessary, expensive, and inconsistent regionally. Additionally, safety and reliability requirements in urban settings mandate that vehicles be able to handle bad weather, complex traffic conditions, and human behavior.

For example, General Motors subsidiary Cruise paused its entire robotaxi operation shortly after an incident involving a pedestrian in 2023. This event prompted debate about how ready we are for autonomous vehicles and emphasized the delicate relationship between public perception, safety, and regulation.

These challenges continue to delay robotaxi market penetration and the establishment of a viable roadmap for a profitable sector. Governments and the private sector will need to continue to support the significant financial investment necessary for long-term solutions.

Like this article? Check out our other Harsh Environment and Commercial Aviation articles, our Transportation Market Page, and our 2025 Article Archives.

Subscribe to our weekly e-newsletters, follow us on LinkedIn, Twitter, and Facebook, and check out our eBook archives for more applicable, expert-informed connectivity content.

- Robotaxis: The Evolution from Hype to Reality - September 30, 2025