OFC/NFOEC Showcased Leading Connector Suppliers

OFC/NFOEC Showcased Leading Connector Suppliers

While this year’s OFC/NFOEC had an underlying theme of Software Defined Networks (SDN), plenty of activity surrounded optical connectivity products. The top connector suppliers have been in and out of the optical interconnect business over the last 10 years. During the optical boom days of the late 1990s and early 2000s, they had varying degrees of optical transceivers, connectors, and cable assemblies, and those that did not were constantly trying to enter the market. They, as well as many analysts, saw it as a potentially lucrative business, if not the entire future of connectivity. Those products and businesses were liquidated when the telecom market tanked, but over the last four years, many have re-entered, for the same reasons as before — they see the dwindling capability of copper interconnects for higher data-rate applications. Thus, with new optical products, it makes sense to showcase them at the largest optical components and networking exhibition in the world, OFC/NFOEC.

Last year many of them had their own booths, including Corning, FCI, Molex, Samtec, and USConec, while others, like Amphenol, TE Connectivity, and Volex, chose to participate in industry group booths like the Ethernet Alliance (EA) and Optical Internetworking Forum (OIF). This year, Amphenol and TE Connectivity not only participated in the EA and OIF booths but added their own displays as well. Regardless of their level of participation, the connector companies we consider the most influential in the industry were present.

The Conference

OFC/NFOEC is the world’s largest conference that includes optical communications technologies. As in years past, both technical and market-driven papers were presented. The technical series included short courses, workshops, tutorials, and technical sessions. The more market-driven material was viewed at the executive forum or on the show floor. Connector companies had presentations in all of these venues. Subjects ranged from the EA panel on “Trends in Interconnects & Integration: Chasing Electrical to Optical Conversion,” on the show floor to a technical session paper on wave-division-multiplexing passive-optical networking (WDM-PON).

The Exhibit Floor

Six of Bishop’s top 10 connector companies (by worldwide sales) showed products on the exhibition floor. Highlights of four of them, plus an up-and-comer, are below.

| Amphenol (#2)Amphenol took part in two demonstrations on the show floor, the Ethernet Alliance (EA) and the Optical Internetworking Forum (OIF), and had its own booth this year. The EA live demo showed multiple data centers interconnected, via 100-Gigabit Ethernet connections across routers from three different equipment manufacturers. Numerous configurations of switches, servers, and test equipment were used within each “data center.” The equipment was connected with a combination of 10G and 40G Ethernet and highlighted some of the breakout cables that make it possible to intermix 10G and 40G in networks today. The OIF showed their new implementation of the next-generation 100G using 25/28G interconnects. Amphenol provided connectors and cable assemblies for both demonstrations.

In its own booth, Amphenol Fiber Optic Products Division highlighted all of its optical connectivity solutions, including those for data centers, wireless communications, and telecom/datacom.

|

|

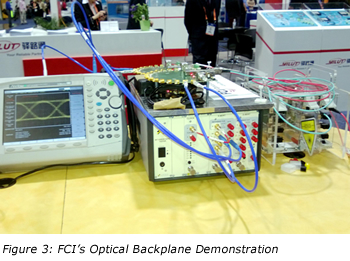

| FCI (#6)FCI had its own booth and was displaying its 40/100G products, new optical miniSAS HD, along with its optical backplane and optical engines. While FCI was a second source to Molex on the miniSAS HD connectors, it seems it is first to market with the optical version of the system. |  |

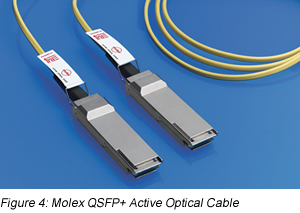

| Molex (#3)Molex was highlighting its AOCs, which use Luxtera’s silicon photonics, along with all of its other optical cable assemblies. There was renewed excitement about silicon photonics with announcements from Cisco and Intel about their commercialization of the technology. Some believe that this will drive an increased interest in these solutions. While Molex does not have its own optical engine, it has a strong relationship with Luxtera and can leverage its silicon photonics optical engine when needed. Molex also participated in the OIFs demonstration. |  |

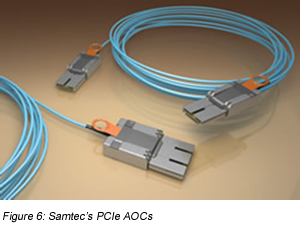

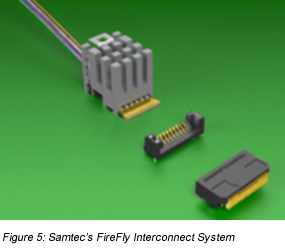

Samtec (#16)Samtec acquired AlpenIO in 2011 and has quickly leveraged its technology into new products. It has brought AOCs to market and with its optical engine has branded a new interconnect system known as FireFly. What should be noted is that Samtec is still the only connector company so far that has figured out how to produce PCIe AOCs, which is one of the applications for the FireFly system.

|

|

| TE Connectivity (#1)In addition to its own booth, TE Connectivity was present in both the OIF and EA booths. It supported the data center demonstration for EA with its cable assemblies and transceivers and the OIF demonstrations of its next generation 100G (4×25/28G) solutions. New this year, TE showed the feasibility of 100G (4x25G) Ethernet. It also showed its new flexible backplane solution, STRADA Whisper, which can actually replace the entire backplane with a cabling solution.

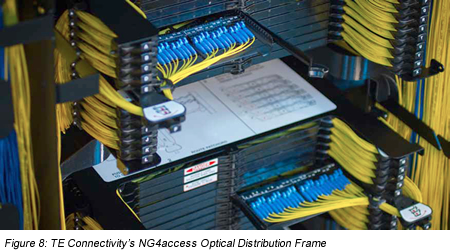

TE Connectivity also has a line of cable management racks (from the old ADC). Its new high-density NG4access optical distribution frame is being used in data centers, central offices, and MSO’s head ends, and was shown in its booth. It boasts more than 3,400 fiber connections.

|

|

Growing Opportunities for Optical Engines

In last year’s article, I showed a forecast for optical engines. Now, there is even more evidence that these devices will become increasingly important in both datacom and telecom networks. With Cisco’s acquisition of LightWire and its announcement of the CPAK module that contains CMOS photonics optical engines, and Intel’s reinvigorated silicon photonics development, the optical engine market growth will be fueled by more than the traditional III-V semiconductor materials, like InP and GaAs. The connector companies that have or are developing optical engines using these traditional high-speed ingredients include FCI, Samtec, and TE Connectivity, while Molex chose the silicon photonics route via Luxtera’s devices.

Optical engines have been around for many years, and are increasingly being utilized in applications in chip-to-chip, board-to-board, and optical backplanes, in addition to their common use as building blocks for optical transceivers such as the SFP+, QSFP+, and CFP modules.

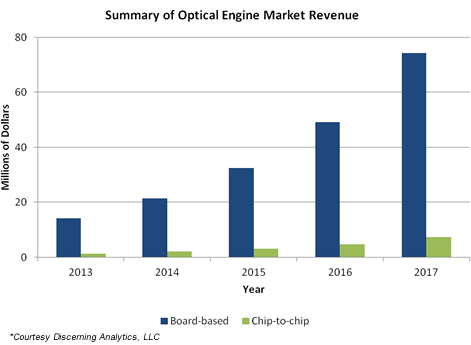

The chart below shows the small but growing market for these products.

While copper datacom and telecom connectors will remain the norm for several years to come, as we move through 40/100G and with 400G on the horizon, there is increasing evidence that more and more of the network will need to become optical. The challenge for the connectivity vendors will be to keep up with their transceiver and systems suppliers, who will be vying for the same revenue.