Slowdown in the Industrial Market? Cable Assembly Suppliers See Dips

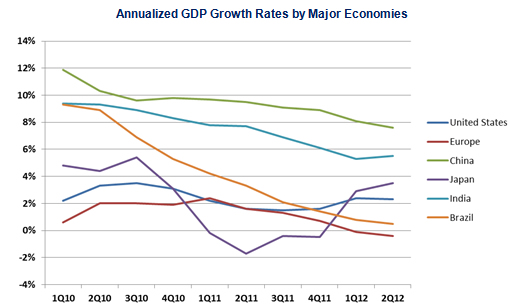

The industrial market experienced good growth over the last two years as the worldwide economies emerged from the recession. The growth has been fueled by nations’ (relatively) recovering economies as well as the need for new equipment after two years of austerity spending. The growth, however, is leveling off, as seen below in a graph that depicts the GDP annual growth rates of six major world economies since the first quarter of 2010.

In developing economies that have had high GDP growth after the recession, such as China, India and Brazil, the drop-off is fairly dramatic. With the exception of Brazil, however, these economies are still growing at a much higher rate than the Western economies, and the developing economies had substantial growth during the recession. As a result, these economies have continued to purchase industrial equipment, such as Caterpillar’s earth-moving equipment, even as their growth slows.

The Western economies, on the other hand, experienced a substantial drop in their GDPs during the recession and spending for industrial equipment was sharply curtailed. Companies in these economies had large year-over-year increases in 2010/2011 relative to their 2008/2009 sales. As a result, with a downturn in the Western economies, such as we currently see in Europe, spending for industrial equipment is dropping quickly.

Bishop tracks 13 market sectors for electronic interconnects. The combined annual revenue of all the market sectors was $4 trillion in 2011 and grew 9.7% over 2010. Of the 13 market sectors, industrial was the fifth fastest growing sector in 2011 at 11.9% year-over-year and combined revenues of $545.8 billion. Profitability was up 35.9% year-over-year to $44.8 billion and sales growth was well above 2010, growing 6% year-over-year.

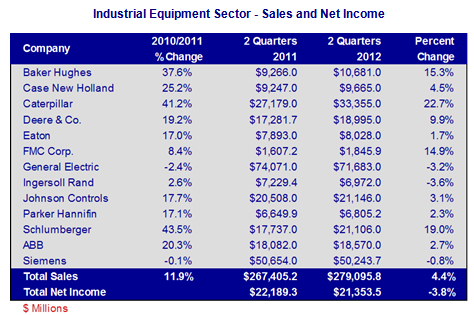

For the industrial market sector, sales for the first half of 2012 increased 4.4%, year-over-year, compared to 2011; sales were up sequentially in 2Q12 versus 1Q12; and net income as a percentage of sales totaled 7.7% for the first half or 2012, down 3.8% year-over-year.

Caterpillar had the largest year-over-year increase in sales for the first half of 2012 at 22.7%, with particularly strong construction equipment sales into China. Schlumberger’s sales were up 19% year-over-year and Baker Hughes was up 15.3%. These last two companies are benefitting from the strong energy market. Additionally, FMC, a diversified chemical company serving agricultural, industrial and consumer markets, recorded sales up 14.9% year-over-year for the first half. Deere & Company sales were up 9.9% year-over-year on their agricultural and construction equipment.

Several of the traditional industrial companies, however, experienced low single-digit growth or decline for the first half of 2012 year-over-year. These include Eaton at 1.7%, Johnson Controls at 3.1%, Ingersoll Rand at -3.6% and General Electric at -3.2%. ABB and Siemens, both European companies, had mixed results at 2.7% and -0.8% respectively.

As can be seen in the following chart, year-over-year sales in the industrial market decreased in 2Q11 through 4Q11, and have been flat in 2012. Sequentially, second quarter 2012 sales increased 2.5% from the first quarter of 2012.

Impact on the Cable Assembly Industry

Bishop projects the worldwide market for industrial cable assemblies to grow 3.3% for 2012. What happens in 2012 and beyond is dependent on social, economic, and political factors worldwide. Some observations:

- Europe has had two quarters of GDP contraction in 2012. It looks likely that this recession will continue through 2012 impacting all market sectors in Europe.

- Automobile sales are down in Europe and production of cars is likely to finish the year 8% to 10% below 2011. Automobile production is a major source of business for the industrial market. The industrial market will have to look to China, Asia Pacific and North America for growth. Automobile sales and production are stronger in these regions.

- Year-to-date, the interconnect industry is down double-digits in Europe and it is expected to stay in that range for the second half of 2012.

- Although their growth is slowing, China and Asia Pacific, are still experiencing growth of 5% to 8%. This area should continue to have respectable growth through the remainder of 2012 and provide a good opportunity for industrial cable assemblies.

Bishop & Associates projects the worldwide market for industrial cable assemblies to be flat at $13 billion in 2012. Europe is the key downside component, which will be countered by growth in China and Asia Pacific, where the expansion will be between 9% to 12% year-over-year, and some help from growth in North America.

- The Outlook for the Cable Assembly Industry in 2021 and Beyond - May 18, 2021

- A Data-Hungry World is Driving Demand for Wireless Connections - January 26, 2021

- Innovation and Expansion Drives Growth of Global Cable Assembly Market - May 7, 2019