Market Facts – Wind Energy

Market Facts – Wind Energy

Wind energy refers to the process by which wind turbines convert the movement of wind into electricity. The rotors of wind turbines transform the kinetic energy of the wind into mechanical energy, and then into electricity.

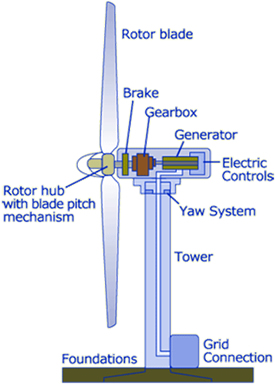

At 100-plus meters (300+ feet) or more above ground, wind turbines are mounted on a tower to capture the faster and less turbulent wind. The nacelle contains the large primary components and is positioned at the top of the tower. The rotor is attached to the front of the nacelle from which power is transferred through a gearbox to a generator. The tower is used to guide the cables from the nacelle down to a transformer, and eventually into the grid network.

At 100-plus meters (300+ feet) or more above ground, wind turbines are mounted on a tower to capture the faster and less turbulent wind. The nacelle contains the large primary components and is positioned at the top of the tower. The rotor is attached to the front of the nacelle from which power is transferred through a gearbox to a generator. The tower is used to guide the cables from the nacelle down to a transformer, and eventually into the grid network.

Most of the current turbine models make best use of the constant variations in the wind by changing the angle of the blades through “pitch control,” by turning or “yawing” the entire rotor as wind direction shifts. Operation at variable speed enables the turbine to adapt to varying wind speeds and increases its ability to harmonize with the operation of the electricity grid. Sophisticated control systems enable fine-tuning of the turbine’s performance and electricity output.

Wind Energy Market Sectors

Wind energy has two distinct market sectors: onshore wind and offshore wind. Onshore wind can be further divided into small-scale and utility-scale wind systems.

The majority of all small-scale turbines built are destined for stand-alone power systems at remote sites. Total installed capacity of small-scale (

For utility-scale (megawatt-sized) sources of wind energy, several hundred wind turbines are usually built close together to form a wind farm. They are controlled and operated through SCADA (supervisory control and data acquisition) systems. A 3 MW class is now considered the standard, while turbines as large as 15 MW are in development.

Offshore wind energy currently accounts for approximately 2% of the total installed wind energy capacity in the world. Over 90% of the development of global offshore wind to date has been around the North and Baltic Seas, and the English Channel. The major challenge for offshore wind is to bring down costs. Selection of sites in deeper waters and farther from shore have contributed to driving the costs up faster than the technology has been able to drive them down.

Regional Wind Energy Market Highlights for 2011

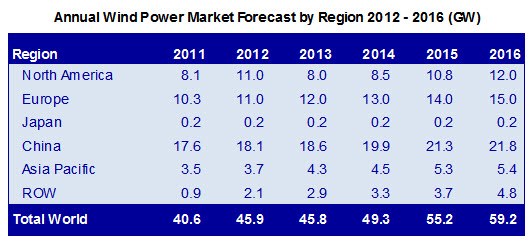

Installed wind power capacity grew in 2011, despite the state of the global economy. An estimated 40 GW of wind power capacity was put into operation in 2011, more than any other renewable technology, increasing global wind capacity by 20% to approximately 238 GW. Total existing wind power capacity by the end of 2011 was enough to meet an estimated 2-3% of global electricity consumption.

China, the US, India, Germany, and the UK, followed closely by Canada, were the top countries for new installations. Japan saw a decline in its renewable energy segment, mostly attributed to resources and attentions diverted by the nuclear disaster and recovery efforts. The EU represented 23% of the global market and accounted for 41% of total global capacity, down from 51% five years earlier.

In 2011, Vestas (Denmark) remained the top wind turbine manufacturer in the world. The remaining top 10, in order, are Goldwind (China), GE Wind (US), Gamesa (Spain), Enercon (Germany), Suzlon (India), Sinovel (China), United Power (China), Siemens (Germany), and Mingyang (China). The key players in the wind energy supply chain are expected to shift over the next year as companies realign their renewable strategies.

Connectivity in Wind Energy

A modern utility-scale wind turbine is a sophisticated, highly precise machine with extreme requirements for temperature, humidity, weight, mechanical stress, and vibration. A single wind turbine may have more than 10,000 mechanical and electrical parts. Water and corrosion are some of the largest threats to safe and reliable  connections in wind-powered operations.

connections in wind-powered operations.

Interconnect content is abundant throughout a wind farm, including the major components inside a wind turbine, the control center, and power collection system. The number of connectors used in a wind turbine varies according to turbine size, application, and location. High-reliability modular interconnects providing “plug-and-play” capabilities are prevalent in the yaw and pitch control systems. At least 25% of the overall wind turbine content is comprised of fiber optic connectors and cable assemblies.

Examples of interconnects used in wind turbine applications include industrial circular, heavy duty, high voltage, high-performance signal and power, M8, M12, and M23 sensors, Industrial Ethernet, and terminal blocks. Cable assembly solutions include data transfer, power distribution, control and monitoring, fiber optic single-mode, and multimode. There are also a wide variety of electrical and mechanical connectors.

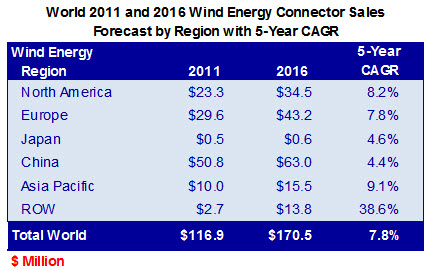

The world total value of electronic connector sales to the wind energy market was $116.9 million in 2011, up 6% from the previous year. The five-year forecast for the wind energy market is $170.5 million in 2016, representing a five-year CAGR of 7.8%.

Market Outlook for Wind Energy

The aftershocks of the credit crisis, the continuing euro zone crisis, and regulatory and political turmoil in Europe and North America continue to hinder the industry. Companies are paring down their development portfolios and rationing costs in the face of regulatory uncertainty, lower energy prices, and depressed energy demand. The continued piecemeal extension of the Production Tax Credit (PTC) in the US is having dramatic effects on the global wind sector. In China, increasing economic imbalances are impacting the ability of the banks to invest in renewable energy.

Market analysts forecast that 2012 will show a record-breaking pace of installations, as developers complete funded projects. There will be a drop in 2013, as there is limited visibility on what will be built. The market will recover and grow through 2016, with an average annual market growth rate of slightly below 8% over the next five years. New emerging markets in Eastern Europe have high potential. Canada, Australia, Brazil, and Mexico could also add considerable growth to global figures.

No part of this article may be used without the permission of Bishop & Associates Inc.

If you would like to receive additional news about the connector industry, register here. You may also contact us at [email protected] or by calling 630.443.2702.

- What is a MIL-DTL-28748 Connector? - July 21, 2026

- Omniball®: Reliable Connections for Challenging Designs - May 19, 2026

- Meet BMF: Powering High Precision, Micro-AM Innovation Across Industries and the Globe - May 13, 2026