Semiconductors Drive the Electronics Industry

Semiconductors drive the electronics industry, and the connection between semiconductors and connectors spans more than three decades.

The semiconductor industry has grown from roughly $10B in 1980 to $300B in 2013. Along the way it transitioned from analog to digital, ECL and Bipolar to CMOS, and has featured sizes from 100s of nm to as low as 20nm.

The semiconductor industry has grown from roughly $10B in 1980 to $300B in 2013. Along the way it transitioned from analog to digital, ECL and Bipolar to CMOS, and has featured sizes from 100s of nm to as low as 20nm.

Its combined 33-year growth rate from 1980 is +11%/year, but its average growth has been slowing dramatically: +22.2% per year from 1980-1990; +16.9% per year from 1990-2000; +5.5% per year from 2000-2010; to +1% per year from 2012-2013.

Semiconductor growth was driven by increasingly smaller feature sizes via better photolithography techniques, advanced semiconductor equipment, semiconducting materials advances, and the compelling fact that ICs could be mass-produced from a single chip design diffused hundreds to thousands of times at once on a silicon wafer. Wafer sizes increased, too, so that more devices would fit on a single wafer.

This cookie-cutter approach yields thousands to millions of identical devices – on a cost curve that has dropped more than 90%. No other product in history has had such a resounding success in productivity – contributing greatly to the growth of the world’s economies and many market segments from consumer to automotive and all other electronic equipment segments.

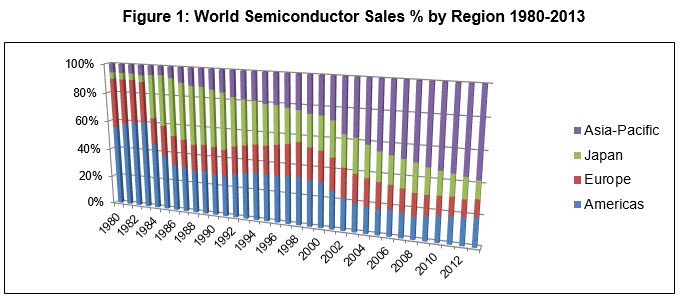

The industry has also globalized. While most of the advanced technology resides in Japan and the West, the Asia-Pacific region, including China, has become a major factor in manufacturing, driven by more commodity-like products such as DRAM, Flash memory, and IC foundry operations. Commodities such as Flash are quite sophisticated, leading-edge designs – but they are industry-standard devices with a steep cost curve, somewhat similar to Hard Disk technology. The chart below is quite dramatic, and emphasizes the difference between technology development and commercialization in a high volume marketplace:

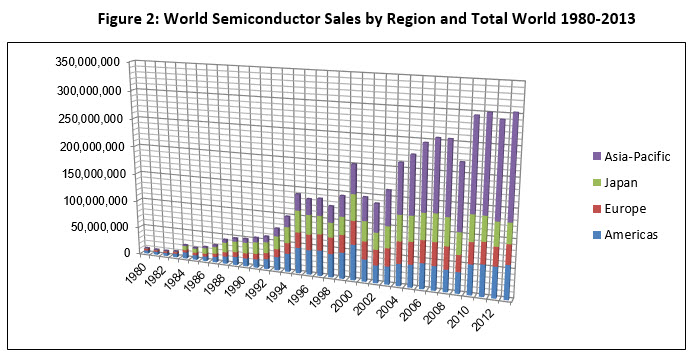

A second chart shows the absolute growth by region over the past 33 years, illustrating that the semiconductor market is, in fact, growth cyclical with four major recessions since 1984:

Semiconductor Scaling Limit?

Conventional CMOSIC technology is approaching its size limits – somewhere in the range of 10nm – where you can actually count the number of atoms. Imaging technology advances have been the key as well as materials advances to current-day IC technology. However, as minimum feature size limits approach, some other technologies will have to step in to maintain Moore’s Law scaling. There are a number of possibilities but what that will be won’t be known for some time. The industry is targeting the mid 2020s when that new technology must be in production.

But here is a hard, cold fact: Semiconductor equipment investments now run into the billions of dollars. Fewer and fewer companies have the financial resources to cope with these numbers and even fewer want to throw out most or all existing investments for a new technology. In addition, you can’t invent some new particle technology smaller than the atom.

Therefore, my prediction is that the essentially planar IC design will go 3D, packing more and more circuitry into a single chip or multiple chips stacked like deck of cards. That is beginning to happen now and will accelerate into the 2020s.

Bottom Line:

- IC scaling will progress into the early 2020s. Beyond that will require one or more new technologies. Moore’s Law as we have known it is approaching its limits.

- There will be fewer top-line IC manufacturers due to huge investment costs. IC manufacturers are partnering to share capital investments.

- The major shift in IC technology now will be to multilayer and stacked chip packaging.

John MacWilliams, Market Director, Bishop & Associates, Inc.

- Electric Vehicles Move into the Mainstream with New EV Battery Technologies - September 7, 2021

- The Dynamic Server Market Reflects Ongoing Innovation in Computing - June 1, 2021

- The Electronics Industry Starts to Ease Out of China - November 3, 2020