Tablets, Nablets, and Phablets Change the Computing Landscape

Since the introduction of the iPad less than five years ago, how, when, and where we compute has changed dramatically. Now, as the handheld technology continues to evolve, tablets, nablets, and phablets will once again change the computing landscape.

Over the past 5 years or so, tablets have been all the rage in the personal systems area. That may be changing – or more accurately, morphing.

Over the past 5 years or so, tablets have been all the rage in the personal systems area. That may be changing – or more accurately, morphing.

We can thank Apple for this new decadal tablet phenomenon: Apple developed the iPad and it took off like an ICBM, cannibalizing segments of the desktop and laptop markets – including that of Apple’s own MacBooks.

The reason for the tablet’s success is that the continued double-digit growth in notebooks was largely due to a significant percentage of sales by consumers, most of whom use the PC light projects. AOL capitalized on this for years, taking most of the mystery out of PCs so long as you stayed on its site. We don’t know whether Steve Jobs recognized this confluence of weaknesses, but his quest for the ultimate user appliance resulted in a device that met 90% of what consumers needed without all the bells and whistles of a PC. Many consumers and some businesspeople ditched their PCs or became first-time buyers of iPads, on which they could read and send email, use touchscreen technology rather than extra external accessories, and expand their horizons with e-books, movies, games, and other applications, including business-related ones.

Of course competition has followed, primarily from Google Android tablets made by Samsung and others. Soon the tablet craze expanded to more than 20 suppliers, mostly from Asia. Interestingly – and perhaps a sign of aging Silicion Valley ingenuity – the major PC suppliers (Dell, HP, Microsoft, and Intel) were slow to react.

This was partly due to PC suppliers’ dependence on “Wintel” to drive the market and innovate for them. They waited, because Microsoft waited, and Intel was still protecting its massive stake in desktop and notebook CPUs. Intel and Microsoft are two fine companies and among the greatest of all time, but as times change, even the most powerful can be slow to react – sometimes for good reason. Both have been, and will be, forces to be reckoned with in this new mobile paradigm.

In addition, there is an extensive eco-system needed beyond hardware to achieve a high market share in tablets. Google solved this for Android tablet makers, while the newer Windows tablet version from Microsoft/Nokia still lags, as would be expected of a late entry with smaller volume.

Then, the “comeback”: Notebooks morphed into “nablets,” slim Ultrabook-style PCs with detachable keyboards, some with magnetic-activated pogo-pin keyboard connectors. These purport to provide the best of both worlds: PC power and applications with tablet functionality. Windows 8, after initial user pushback, handsomely provides an alternative touchscreen experience with notebook or desktop power. The Microsoft Surface 3 exemplifies this trend with Core i7 power in a 12” ultra-high-resolution convertible notebook with solid-state storage.

The only problem with this – if there is one – is that these nablets are priced close to the $1,000 notebook market, not $500 consumer tablets. What they do is (hopefully) prevent business users from straying back to a tablet; they may take away more from the traditional notebook market than from tablets but with fewer I/O ports and internal connectors. An alternative is the use of a tablet with an external Bluetooth keyboard/stand combo. They work great with Windows, Android, or iOS tablets. Logitech and others do a fine job with this must-have tablet accessory.

So what does this mean for the tablet and laptop markets?

- Tablet sales may have peaked, or at least are registering slower growth rates. Apple registered 5% declines the past two quarters, perhaps because Samsung has caught up and Apple’s pricing is stiffer. The reason also appears to be that the market is nearing saturation and will need another breakthrough to regain double-digit growth. There will be a Christmas 2014 seasonal push, and new products are in the offing. Plus, tablets are a replaceable commodity due to their lower price points.

- Smartphone sales may also be peaking, except for the iPhone, which is gaining ground in China and elsewhere in the developing world. Phones are getting bigger and some rival smaller tablets in size. The anticipated 5.5” iPhone 6 “phablet” will eat into tablet sales, and 6” Windows phones are already available. So the whole market seems to be converging in on itself, from slim Ultrabooks to nablets, tablets, and phablets to mobile phones. It’s a sign of the digital convergence of the consumer market segment.

- This in turn results in very short product life cycles, or at least a rapid growth stage as a prelude to maturity, easily less than five years. With standardization on the lightning connector, micro-SD, micro-SIM, and USB, the I/O connectors are less affected. Internally the designs do change, with each iteration becoming more highly integrated with powerful multi-core CPUs, SiP/3D device-integration, and surface-mount flash memory.

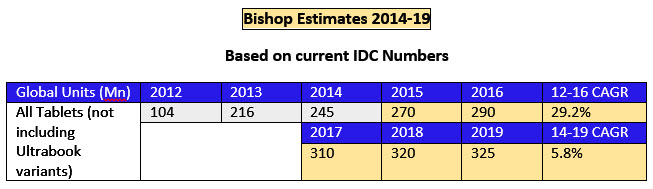

Tablet Sales in 2014 are forecast by IDC to increase to 245 million units, just 12% over 2013, down from a 52% increase in 2013 and triple digits before. IDC predicts that larger tablets will do better, while smaller ones will be affected by larger-screen smartphones.

Our prognostication for the next five years is as follows:

If a breakthrough tablet-type product should occur, which is probable based on the dynamics of this category, these forecast rates will increase. In addition, tablet and Ultrabook forecasts will merge – including larger tablet-phones, being bifurcated into large 7” or greater and 5.9” or smaller tablet/phablet designs. In any event, the future looks fuzzy but a bit more down to earth, meaning we’ve probably seen most of the major tablet innovations on deck for a while; the strong will survive in developed world markets, but there may still be room for newcomers and smaller entrants, particularly in Asia. In addition, don’t rule out Lenovo….

In the connector industry, for those able to compete with Asia in the high-volume consumer segment, there will continue to be high-volume applications for the Lightning connector (Apple), Micro-USB, Micro-SD, SIM, and other I/O connectors (Samsung and others); microminiature board-to-board and FPC connectors (both); battery connectors (Samsung); and external charging/docking connectors and cables (both). Assuming 12 total average per system, tablets in 2014 will consume almost three billion connectors, a fair amount, and close to four billion connectors in 2019.

John MacWilliams, Market Director, Bishop & Associates, Inc.

- Electric Vehicles Move into the Mainstream with New EV Battery Technologies - September 7, 2021

- The Dynamic Server Market Reflects Ongoing Innovation in Computing - June 1, 2021

- The Electronics Industry Starts to Ease Out of China - November 3, 2020