The Server Market for Connectors

The Server Market for Connectors

Servers are defined as a computer dedicated to serve the requests of users. The server performs computational, file, or application tasks for the client (individuals, workgroups, and organizations).

Servers were developed as the computer market shifted away from mainframes and minicomputers to PCs, networks, and the Internet. This sea change gave birth to a growing variety of server systems, including volume/blade servers, departmental servers, enterprise servers, and many Internet-centric server products. Application servers include database servers, file servers, mail servers, print servers, and web servers (or multi-application virtualization servers). Servers can also be classified by architecture: X86, RISC/Unix, and proprietary. X86 servers tend to be entry-level to midrange; RISC/Unix servers at the mid-to-high end. Mainframes still exist for large centralized corporate users, led by IBM. Minicomputers, such as those from DEC and Data General, are essentially gone, gobbled up by the relentless shift to PCs and network computing.

There are similarities between servers and PCs as well as between servers and mainframes. Typically, servers use similar components and subsystems, yet there are more of them, and many have proprietary system architecture. Servers do not typically have the sheer computational power of mainframes or scientific computers, but are strong on multi-processors, large memory banks, Hard Disk Drive (HDD) storage, high-speed IO, and fault-tolerant capabilities. Components used in servers are usually high quality, source-restricted, and meet higher performance requirements. Since a server outage can cost more than the system itself, cost is less of a factor than in commodity PC products.

Server Market

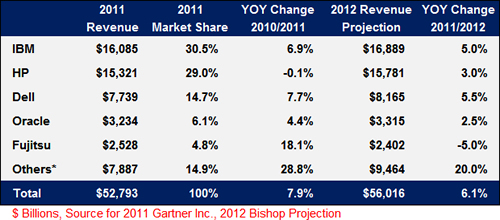

The $52.7B server market has a nominal 5-7.5% AGR but is sensitive to economic cycles. According to Gartner, 2011 was led in revenues by IBM (33.7%), followed by HP (26.9%), Dell (14.6%), Oracle-Sun (5.3%), Fujitsu (3.6%) and all others (15.8%). The market in 2012 appears to be weaker, particularly in Europe.

The market for the year 2011 increased 7.9% in value, but declined 5% in 4Q11, and grew 1.5% in 1Q12. Prospects for the remainder of 2012 are mixed. Of particular concern is a slowdown in Europe caused, in part, by the continuing fiscal crisis there. IT spending is forecast to increase 3% in 2012 to $3.6 trillion. At that rate, total server shipments will represent approximately 2% of total IT spending.

The market is dominated by the North American suppliers mentioned above. IBM, HP, and others have their own factories in the United States and Europe. Other companies outsource to leading EMS suppliers. The dynamics of this competition are as follows:

- Intel remains strong due to its Xeon and other CPUs, chip sets, motherboards, and overall influence on X86 server designs.

- Microsoft also remains a strong, non-hardware influence with their Windows NT and Server 2012 software.

- HP has stumbled a bit with corporate shakeups and its announced downsizing.

- Dell has focused on servers to shore up its profitability and it is clear that its financial strength will depend on server business.

- IBM moves along, remaining the industry leader in dollars and profitability.

- Sun is stable under its new Oracle ownership and still has a strong following in the IT industry.

- Lenovo is emerging as a force in China and will become an increasing factor in that market.

- Low power/micro-server technology may result in the next sea change in the server market.

- Server virtualization can cannibalize servers at a 10-to-1 ratio where it is deployed and is a serious emerging factor.

- Cloud computing is a major shift, with companies like Rackspace offering remote server/storage “in the cloud.”

- Solid-state disks are coming with their low power and fast access times and will complement HDDs in server/storage markets.

Table 1. 2011/2012 World Server Market by Manufacturer

Connector Products Used in Server Systems

Starting with CPUs, typically two to 16 chip-sets are used per system (and up to 32/system). These chips are mostly socketed with PGA or LGA high pin count sockets with chips supplied by Intel, AMD, and proprietary RISC designs. There is a trend toward very low power CPUs, and many of these will be direct-attached to logic boards. With these low power chips, in the future there could be hundreds of CPUs/system. Memory is usually DDR3, with DDR4 not going mainstream until 2015. Depending on the application, there can be four to 12+ DIMM sockets per system. Backplane connectors are used in rack/blade and high-end systems as Ethernet networking surpasses 10Gbps and approaches 40 Gbps. Numerous other connectors are used, including PCIe, SATA, or SAS/SCSI variants for HDD applications, with Solid-State Drives (SSD) beginning to make inroads to complement HDD applications. SATA could be superceded by the small form factor working group with a higher speed interface. Electronic Power/Blade Connectors are also used extensively in high-end systems. High-speed cabling is common and dense, including SFP/QSFP, active fiber optic cables, and Infiniband connections. Rack and equipment room cabling is intense as I/O speeds increase, with tons of RJ45/Cat5-7 and coaxial/twinaxial cabling. Fiber optics is used in high-end applications, including rack-to-rack and intersystem/equipment room/LAN/WAN cabling. Connector BOMs vary from PC-look-alike, low-end systems through blade servers to massive enterprise systems.

Starting with CPUs, typically two to 16 chip-sets are used per system (and up to 32/system). These chips are mostly socketed with PGA or LGA high pin count sockets with chips supplied by Intel, AMD, and proprietary RISC designs. There is a trend toward very low power CPUs, and many of these will be direct-attached to logic boards. With these low power chips, in the future there could be hundreds of CPUs/system. Memory is usually DDR3, with DDR4 not going mainstream until 2015. Depending on the application, there can be four to 12+ DIMM sockets per system. Backplane connectors are used in rack/blade and high-end systems as Ethernet networking surpasses 10Gbps and approaches 40 Gbps. Numerous other connectors are used, including PCIe, SATA, or SAS/SCSI variants for HDD applications, with Solid-State Drives (SSD) beginning to make inroads to complement HDD applications. SATA could be superceded by the small form factor working group with a higher speed interface. Electronic Power/Blade Connectors are also used extensively in high-end systems. High-speed cabling is common and dense, including SFP/QSFP, active fiber optic cables, and Infiniband connections. Rack and equipment room cabling is intense as I/O speeds increase, with tons of RJ45/Cat5-7 and coaxial/twinaxial cabling. Fiber optics is used in high-end applications, including rack-to-rack and intersystem/equipment room/LAN/WAN cabling. Connector BOMs vary from PC-look-alike, low-end systems through blade servers to massive enterprise systems.

The number of connectors per system ranges from 20 to 30 in lower-end systems and blade servers to 50 to 100 in high-end systems. Since many server applications involve multiple racks, the number of connectors and cable assemblies used in equipment room applications reach the hundreds. There is a mixed bag in connector sourcing, but the strong US server OEMs tend to control their BOMs both in-house and with EMS suppliers.

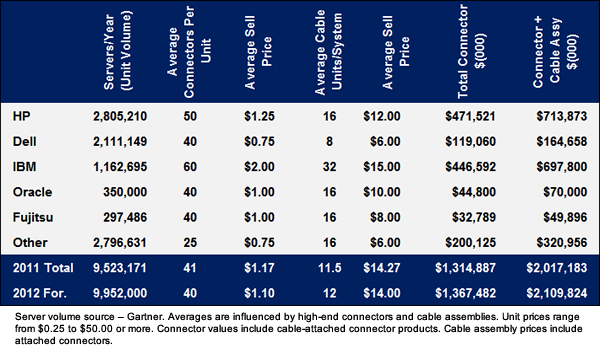

An estimate of the number of connectors and cable assemblies used by each OEM is shown in table 2 for 2011 and 2012.

Table 2. 2011 World Interconnect Value by Server OEM

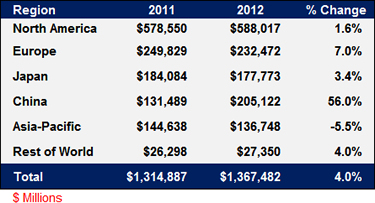

The following table shows the breakdown of the server connector content by region of the world.

Table 3. World Server Interconnect Value by Region

No part of this article may be used without the permission of Bishop & Associates Inc.

If you would like to subscribe to the Connector Industry Forecast, go to connectorindustry.com and select “Research Reports.” You may also contact us at [email protected], or by calling 630.443.2702.

- Electric Vehicles Move into the Mainstream with New EV Battery Technologies - September 7, 2021

- The Dynamic Server Market Reflects Ongoing Innovation in Computing - June 1, 2021

- The Electronics Industry Starts to Ease Out of China - November 3, 2020